The Nisshinbo Group's Financial Strategy

Tetsuya Kumakawa

Director, Managing Officer

Introduction

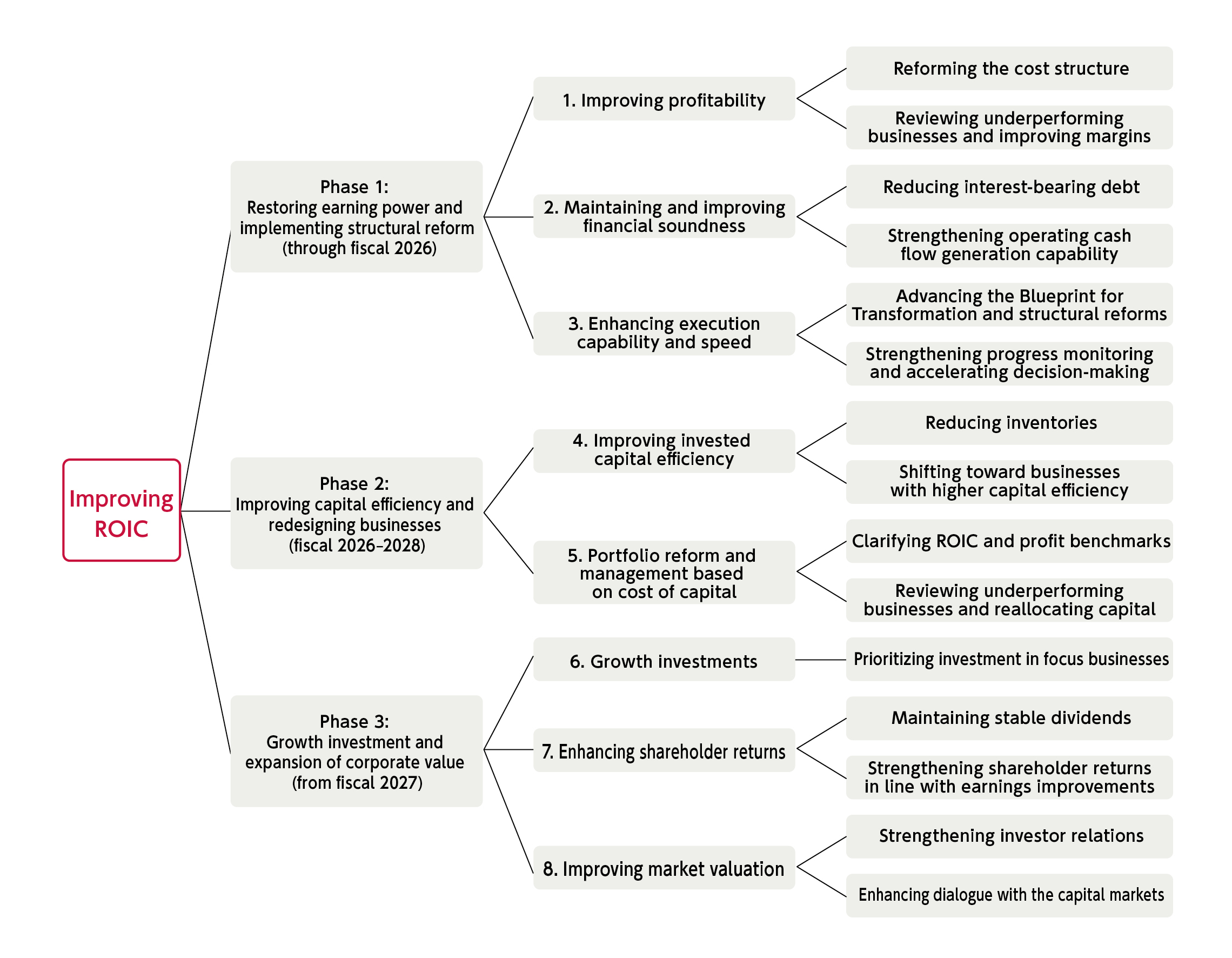

We have begun implementing fundamental reforms to our business portfolio and earnings structure under the Blueprint for Transformation.

Since assuming responsibility for finance and accounting in April 2026, my role as the executive officer overseeing finance and accounting has been to translate this blueprint into capital allocation and financial discipline, and connect it to concrete decision-making and outcomes.

Through my involvement in business operations both in Japan and overseas, I have come to strongly recognize that sustainable corporate growth requires both “earning power” and the optimal allocation of the capital that supports it. The concept of Public Entity that we value is likewise based on the cycle of value creation and redistribution. Going forward, we will translate this philosophy into a more effective financial strategy and execute it with greater speed.

Basic Financial Strategy

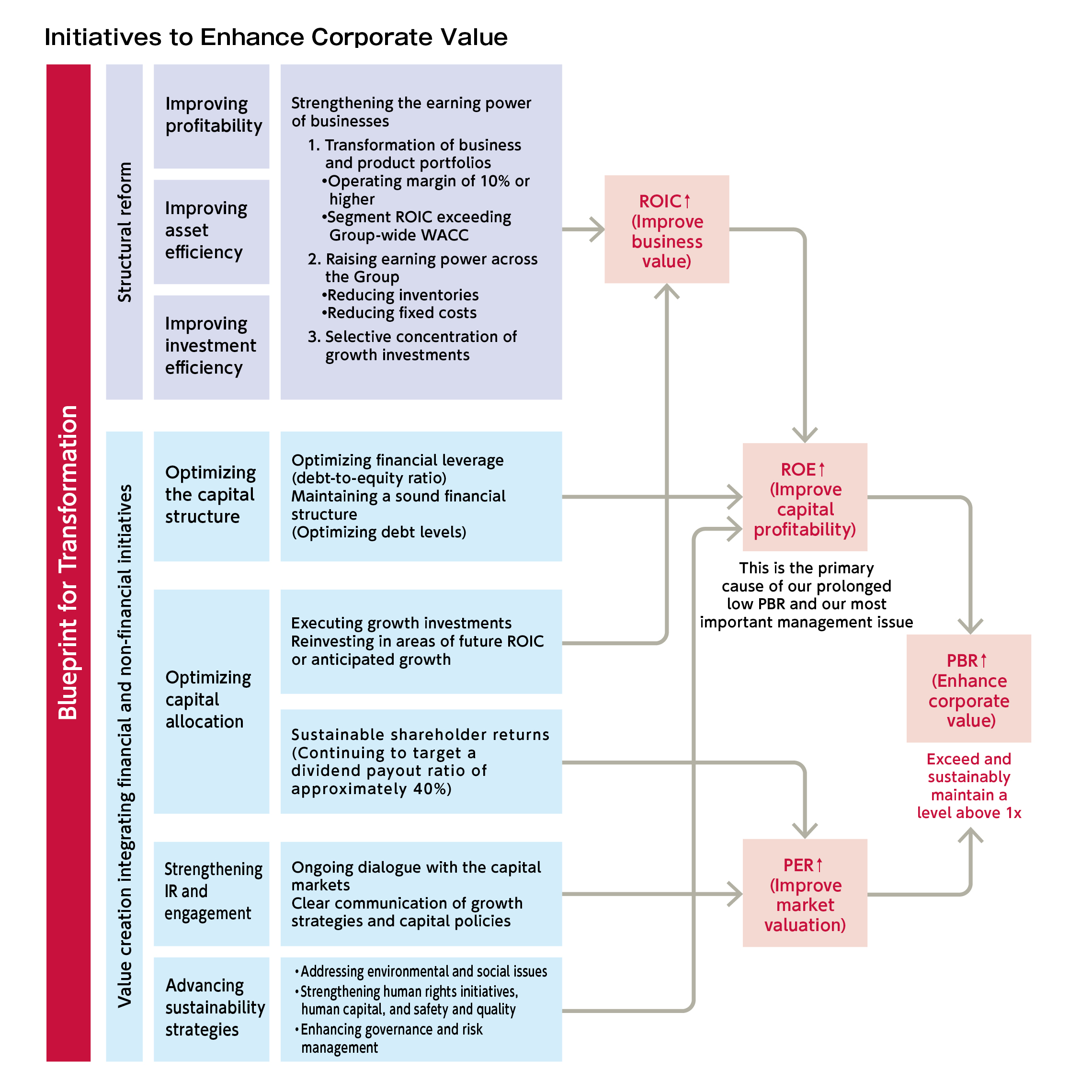

Our financial strategy is centered on improving earning power while achieving both financial soundness and capital efficiency. Recently, interest-bearing debt has increased temporarily due to the progress of structural reforms. However, we will maintain disciplined control over investments within the scope of our cash-generating capacity and optimize debt levels within a funding cycle based on profits and depreciation and amortization. Financial soundness is the result; the foundation supporting it is sustainable profit-generating capability—in other words, “earning power.”

From the perspective of capital efficiency, it is also important not only to improve financial indicators but also to transform our business structure into one capable of sustainably generating returns that exceed the cost of capital. Accordingly, in making investment decisions, we will evaluate profitability, growth potential, and capital efficiency in an integrated manner while optimizing resource allocation.

Fiscal 2025 Performance and Key Issues

In fiscal 2025, we achieved increases in both sales and profits against the backdrop of expanding demand in the Wireless and Communications business. However, this performance was largely driven by the business environment surrounding specific businesses, and we recognize that the Group’s true earning power remains insufficient. In terms of cash-generating capability as well, we see divergence between profits and cash flow, and believe there remains room for improvement from the standpoint of capital efficiency.

In addition, the effects of the structural reforms initiated in fiscal 2025 have so far been limited, and it would not be appropriate at this stage to regard current profit levels as sustainable. There is also room for improvement from a balance sheet perspective, including inventory levels and asset efficiency, and we must improve the quality of our cash flow.

In fiscal 2026 as well, we will prioritize fundamental improvements to our earnings structure and asset efficiency while focusing on building the foundation needed to transition to the next phase of growth.

The targets presented by the president—an operating margin of 10% and an ROIC of 7%—will not be managed simply as numerical goals, but as disciplines for determining whether businesses should continue and grow.

Our current weighted average cost of capital (WACC) is approximately 6%, but we assume it could rise to around 7% in light of future interest rate conditions and other factors. Based on this assumption, for businesses with an ROIC that falls below the cost of capital, we will strictly monitor progress in improvement efforts and, where improvement cannot be expected, execute decisions including restructuring or withdrawal without hesitation.

In evaluating businesses, we will make multifaceted assessments based not only on quantitative indicators such as ROIC but also on qualitative factors including market growth potential, technological advantages, and the competitive environment. We must determine whether a business can continue generating returns above the cost of capital over the long term, and assessing the likelihood of this is one of our most important roles in finance.

In addition, as a conglomerate, our evaluations must consider not only the stand-alone value of each business but also synergies within the Group and the optimal allocation of capital. From the perspective of maximizing corporate value across the portfolio as a whole, we will proceed with restructuring, including portfolio reconfiguration where necessary.

Initiatives to Improve Capital Efficiency and PBR

Our price-to-book ratio (PBR) remained below 1x until recently, and we certainly recognize that we are not receiving sufficient recognition from the capital markets.

To improve PBR, we recognize that the fundamental issue lies in low capital efficiency and that improving profitability through ROIC improvement is the most important driver. Alongside achieving profit growth that does not rely on onetime factors such as real estate sales, we will improve asset efficiency through measures including reducing total assets and inventories, thereby improving return on assets (ROA) and return on equity (ROE).

In addition, when selecting investment projects or making withdrawal decisions, we will apply standards that clearly incorporate awareness of the cost of capital and improve capital turnover. Through these initiatives, we will strengthen our management foundation while carefully communicating our story for enhancing corporate value through dialogue with the capital markets, ultimately leading to improved PBR.

Capital Allocation

Under Medium-Term Management Plan 2026, we formulated plans for cash generation and investment allocation. However, cash generation is currently below plan, and much of the cash generated is being allocated to structural reforms.

While structural reform places short-term pressure on cash flow, we position structural reform as a priority investment for strengthening our earnings base, and we will prioritize it for the time being. Based on this, we expect to accelerate growth investments in earnest from fiscal 2027 onward.

With regard to shareholder returns, while maintaining stable dividends, we aim to increase return levels in line with improvements in “earning power.” There is no change to our basic policy of setting the annual dividend per share at a minimum of ¥36 and targeting a dividend payout ratio of 40%.

After carrying out structural reforms decisively, we will first direct the cash generated toward growth investments, while also considering raising dividend levels in line with progress in “earning power.” What is important is building a financial structure capable of sustainably generating cash while balancing shareholder returns and growth investments.

Relationship between Non-Financial Value and Finance

The source of value creation lies in non-financial areas such as human capital and technological capabilities. We do not view financial value and nonfinancial value as separate, but rather as integrated elements that together form corporate value.

Based on the idea that the company is a Public Entity, we have long valued the philosophy that “business is people,” and have regarded intellectual capital—including human capital and technological capabilities—as the essence of corporate value. Due to accounting rules, the assets recorded on the balance sheet are limited, and many of these sources of value cannot be fully captured through financial figures alone. Going forward, however, we will seek to quantify non-financial indicators wherever possible and appropriately communicate their value through dialogue with the capital markets. Sustainability initiatives not only enhance corporate resilience but also over the medium to long term contribute to reducing the cost of capital.

The Role of Finance

The role of finance is to ensure that the Blueprint for Transformation goes beyond a mere concept and is translated into corporate value through disciplined execution.

Going forward, alongside building the information infrastructure needed to support rapid decision-making, we will thoroughly enforce both investment discipline and withdrawal discipline while practicing management that remains conscious of the cost of capital while balancing growth and risk control.

By achieving both speed and discipline and steadily implementing the Blueprint for Transformation, we will realize sustainable enhancement of corporate value and pursue financial management evaluated based on results.